Liquidation and Partial Liquidation

What is liquidation and why does it happen?

Liquidation is a mechanism designed to protect traders from incurring losses that exceed their margin balance and potentially lead to liquidation(negative margin balance).

To prevent this, the system establishes a minimum margin requirement for each type of contract, known as the maintenance margin. When a trader's margin balance reaches or falls below the maintenance margin requirement, the system initiates the liquidation process.

When a position is liquidated, it is unwound and all of the money from your margin is used to cover the losses - hence making your margin balance go to zero.

What is partial liquidation?

Partial liquidation refers to the process where only a portion of a trader's position is closed to meet the maintenance margin requirements, instead of liquidating the entire position. This helps to minimize potential losses and protects the trader's margin balance from going to zero, while still maintaining a portion of their original position in the market.

What is forced market buying/selling and why does it happen?

Forced market buying/selling refers to a situation in which the trading system automatically executes a buy/sell market order on behalf of the trader, to convert unrealized profits into realized profits.

This typically occurs in scenarios where the trader's position is at risk of liquidation due to insufficient margin or when maintenance margin requirements are not met. The purpose of a forced market buy/sell is to mitigate potential losses and protect the trader's remaining margin balance.

What will happen when liquidation or partial liquidation occurs?

Upon liquidation, the system assumes control of your position and the remaining margin balance, aiming to close the position (or part of it) at the liquidation price.

If the position cannot be closed at the liquidation price, the system seeks additional margin from BTZO's insurance fund to adjust the price further up or down, increasing the likelihood of successfully closing the position.

Should the position remain open after these adjustments, the system initiates the auto-deleveraging (ADL) process. This involves systematically matching the liquidated position with opposite positions to close it off. Both sides' position sizes continue to decrease until the liquidated position is entirely closed.

The priority for auto-deleveraging by the liquidation engine is determined by the profit and leverage levels of the counterparty position(s).

*In Hedge Mode, both your long and short positions in the specified market will be liquidated when liquidation occurs. The partial liquidation process will first try to close your fully hedged position size in the specified market. If the margin balance is still insufficient after closing the fully hedged position size, the non-fully hedged position size will also be liquidated

*In Hedge Mode, both your long and short positions in the specified market will be liquidated when liquidation occurs. The partial liquidation process will first try to close your fully hedged position size in the specified market. If the margin balance is still insufficient after closing the fully hedged position size, the non-fully hedged position size will also be liquidated

How does the system determine when to initiate the liquidation, partial liquidation or forced market buy/sell process?

Upon entering a position, the system calculates a liquidation price for your reference. If the Mark Price crosses your liquidation price, it indicates that your margin balance is insufficient to meet the maintenance margin requirement.

At this point, the system automatically triggers either the liquidation, partial liquidation or forced market buy/sell process, depending on the circumstances.

Mark Price: Acts as a fair price, derived from multiple price sources. To prevent market manipulation and potential liquidation of a significant number of users, BTZO uses the Mark Price as the basis for initiating the liquidation, partial liquidation or forced market buy/sell process.

How can you prevent liquidation and avoid losing more than anticipated?

To minimize the risk of liquidation or losses beyond your expectations, consider implementing the following strategies:

1. Monitor maintenance margin requirements and select a suitable leverage

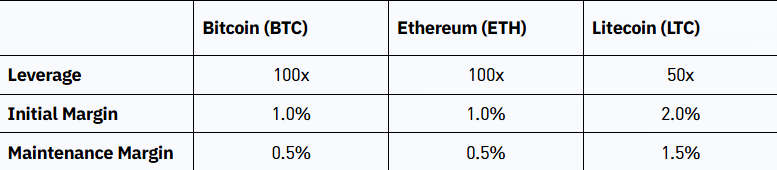

For instance, the BTC perpetual future contracts necessitate a 0.5% maintenance margin of the notional value (the lowest risk limit setting), while the LTC perpetual futures contracts require 1.5% (the lowest risk limit setting). Be aware that different futures contracts may have varying maintenance margin requirements.

Choosing an appropriate leverage is also helpful in avoiding liquidation, because the leverage impacts how likely you are to be liquidated. The higher the leverage, the lower the amount of funds available to use as margin.

2. Track your liquidation price and top up your margin balance as needed

When the Mark Price approaches your liquidation price, add funds to your margin balance to prevent the liquidation price from reaching the Mark Price. You can achieve this by depositing more assets into the specific Futures Wallet.

3. Set a stop-loss point and close your position before liquidation occurs

Designate a TP/SL (Take Profit / Stop Loss) setting or create a Stop-Loss Order in advance. If the market price trend deviates from your expectations, the system will trigger the TP/SL setting or the Stop-Loss Order based on your predetermined trigger price. Be aware that in highly volatile markets, TP/SL may perform as expected.

4. Allocate funds according to the level of risk you are willing to accept

In addition to the above strategies, manage your margin balance to avoid unexpected losses.

For example:

Suppose you earned a profit of 1,000 USDT but are only willing to risk 500 USDT. You can transfer 500 USDT back to your Spot Wallet to prevent unanticipated losses caused by the system automatically replenishing your margin.

How is the initial margin calculated?

Initial Margin = Notional Value x ( Initial Margin% + Taker Fee% * 2 )

Notional Value = Mark Price x Position Size x Contract Multiplier

For example, when you buy long contracts of BTC-PERP with the following conditions:

- Market Price: 40,000 USDT

- Mark Price: 40,001 USDT

- Position Size: 10,000 (contracts)

- Contract Multiplier: 0.00001

- Initial Margin: 1.00%

- Taker Fee%: 0.05%

Given the above conditions, the initial margin of this position will be: 40,001 x 10,000 x 0.00001 x ( 1% + 0.05% * 2 ) = 44.0011 USDT

How is the maintenance margin (position margin) calculated in one-way mode?

Maintenance Margin = Notional Value x ( Maintenance Margin% + Taker Fee% + | Funding Rate% | )

*Assign a 0 Funding Rate % for negative funding rate percentages when holding long positions, and for positive percentages when holding short positions.*

Notional Value = Mark Price x Position Size x Contract Multiplier

For example, when you buy long contracts of BTC with the following conditions:

- Market Price: 40,000 USDT

- Mark Price: 40,001 USDT

- Position Size: 10,000 (contracts)

- Contract Multiplier: 0.00001

- Maintenance Margin: 0.50%

- Taker Fee%: 0.05%

- Fund Rate%: 0.01%

Given the above conditions, the maintenance margin of this position will be: 40,001 x 10,000 x 0.00001 x ( 0.5% + 0.05% + | 0.01% | ) = 22.40056 USDT

Given the above conditions, the maintenance margin of this position will be: 40,001 x 10,000 x 0.00001 x ( 0.5% + 0.05% + | 0.01% | ) = 22.40056 USDT

How is the maintenance margin (position margin) calculated in hedge mode?

Maintenance Margin = min( Long Position Size, | Short Position Size | ) * Entry Price * Contract Multiplier * Rate + ( | Position Size | - min( Long Position Size, | Short Position Size | ) ) * Contract Multiplier * Mark Price * Rate

Rate = Maintenance Margin% + Taker Fee% + | Funding Rate% |

*Assign a 0 Funding Rate % for negative funding rate percentages when holding long positions, and for positive percentages when holding short positions. *

For example, when you buy positions of BTC with the following conditions:

- Market Price: 40,000 USDT

- Mark Price: 40,001 USDT

- Long Position Size: +20,000 (contracts)

- Entry Price of Long Position: 39,000 USDT

- Short Position Size: -10,000 (contracts)

- Entry Price of Short position: 39,990 USDT

- Contract Multiplier: 0.00001

- Maintenance Margin: 0.50%

- Taker Fee%: 0.05%

- Funding Rate%: 0.01%

Hence the maintenance margin of the long position will be:

min( 20000, | -10000 | ) * 39,000 * 0.00001 * ( 0.5% + 0.05% + | 0.01% | ) + ( 20000 - min( 20000, | -10000 | ) ) * 0.00001 * 40,001 * ( 0.5% + 0.05% + | 0.01% | ) = 44.24056

The maintenance margin of the short position will be:

min( 20000, | -10000 | ) * 39,990 * 0.00001 * ( 0.5% + 0.05% ) + ( | -10000 | - min( 20000, | -10000 | ) ) * 0.00001 * 40,001 * ( 0.5% + 0.05% ) = 21.9945

How is the liquidation price calculated in one-way mode?

Liquidation price of long position = (Notional Value - (Available Balance + Position Margin) ) / ( (1-Rate) * Position Size * Contract Multiplier )

Liquidation price of short position = (Notional Value + (Available Balance + Position Margin) ) / ( (1+Rate) * Position Size * Contract Multiplier )

Notional Value = Mark Price * Position Size * Contract Multiplier

Position Margin = Notional Value * Rate

Rate = Maintenance Margin% + Taker Fees% + | Funding Rate% |

*Assign a 0 Funding Rate % for negative funding rate percentages when holding long positions, and for positive percentages when holding short positions.*

For example, you have a BTC Perpetual long position with the following conditions:

- Position Size: 10,000 contracts

- Contract Multiplier: 0.00001

- Entry Price: 40,000 USDT

- Mark Price: 41,000 USDT

- Maintenance Margin%: 0.50%

- Taker Fee %: 0.05 %

- Funding Fee %: 0.01 %

- Available Balance: 300 USDT

Given the above conditions, the liquidation price of the long position will be:

( 41,000 * 10000 * 0.00001 - ( 300 + 41,000 * 10000 * 0.00001 * ( 0.5% + 0.05% + | 0.01% | ) ) ) / ( (1 - ( 0.5% + 0.05% + | 0.01% | ) ) * 10000 * 0.00001 ) = 37,983.10539

How is the liquidation price calculated in hedge mode?

Calculate the Net Position Size first. If the direction of Net Position is long, you can use the long liquidation price formula. If the direction of Net Position is short, you can use the short liquidation price formula.

Net Position Size = Long Position Size + Short Position Size

Liquidation Price of Long Position = ( Net Notional Value - ( Available Balance + Position Margin of Net Position size ) ) / ( (1-Rate) * Net Position Size * Contract Multiplier )

Liquidation Price of Short Position = ( Net Notional Value + ( Available Balance + Position Margin of Net Position size ) / ( (1+Rate) * Net Position Size * Contract Multiplier )

Net Notional Value = Mark Price * | Net Position Size | * Contract Multiplier

Position Margin of Net Position Size = Net Notional Value * Rate

Rate = Maintenance Margin% + Taker Fees% + | Funding Rate% |

*Assign 0 Funding Rate% for negative funding rate percentages when holding long positions, and for positive percentages when holding short positions. *

For example, you have BTC Perpetual Positions with the following conditions:

- Long Position Size: +20,000 (contracts)

- Short Position Size: -10,000 (contracts)

- Contract Multiplier: 0.00001

- Mark Price: 41,000 USDT

- Maintenance Margin%: 0.50%

- Taker Fee %: 0.05 %

- Funding Fee %: 0.01 %

- Available Balance: 300 USDT

Hence the liquidation price of this market will be:

Net Position Size = 20000 + (-10000) = 10000

Net Notional Value = 41,000 * | 10000 | * 0.00001 = 4,100

Rate = 0.5% + 0.05% + | 0.01% | = 0.56%

Position Margin of Net Position size = 4,100 * 0.56% = 22.96

Liquidation Price = ( 4,100 - ( 300 + 22.96 ) ) / ( ( 1 - 0.56% ) * 10000 * 0.00001 ) = 37,983.10539

Related Articles

Perpetual Contracts

What is a Perpetual Contract? A perpetual contract is a product similar to a traditional futures contract in how it trades, but does not have an expiry date, so you can hold a position for as long as you like. Perpetual contracts trade like spot, ...What is One-Way Mode and Hedge Mode

What is One-Way Mode? One-Way Mode refers to a specific position mode setting. When you set your position mode to One-Way Mode, you can only hold one direction, either long or short. This mode offers a straightforward way to manage your position, ...Insurance Fund

BTZO employed the insurance fund system to assist winning traders to realize their full profit and avoid being interrupted by the Auto-Deleveraging events (ADL). The ADL mechanism protect losing traders by ensuring they will never go into negative ...Leverage

Leverage How much leverage does BTZO offer? BTZO offers up to 100x Leverage on its futures products. 100x leverage is offered for Bitcoin and Ethereum, while most altcoins can be leveraged up to 20x. What is Initial Margin? Initial Margin is the ...Index Price and Mark Price

Index Price is an important reference when you are investing. It's the average market price of cryptocurrencies on major exchanges. It’s also the primary component of the mark price. Mark Price is the price used for mark-to-market PnL calculation and ...